Term vs Whole Life Insurance: The Core Trade-Off

Choosing between term vs whole life insurance is one of the most common financial dilemmas. Term life offers pure protection for a set period, while whole life adds a savings component. Your decision impacts your budget, future flexibility, and family’s security.

The term vs whole life debate often centers on cost versus permanence. Many buyers focus on monthly premiums, but long-term value matters just as much.

Understanding the trade-offs will help you pick the right policy.

How Term Life Insurance Works

Term life covers you for 10, 20, or 30 years. If you die within that term, your beneficiaries get the death benefit.

Premiums stay level, and there's no cash value. It's the cheapest way to get substantial coverage.

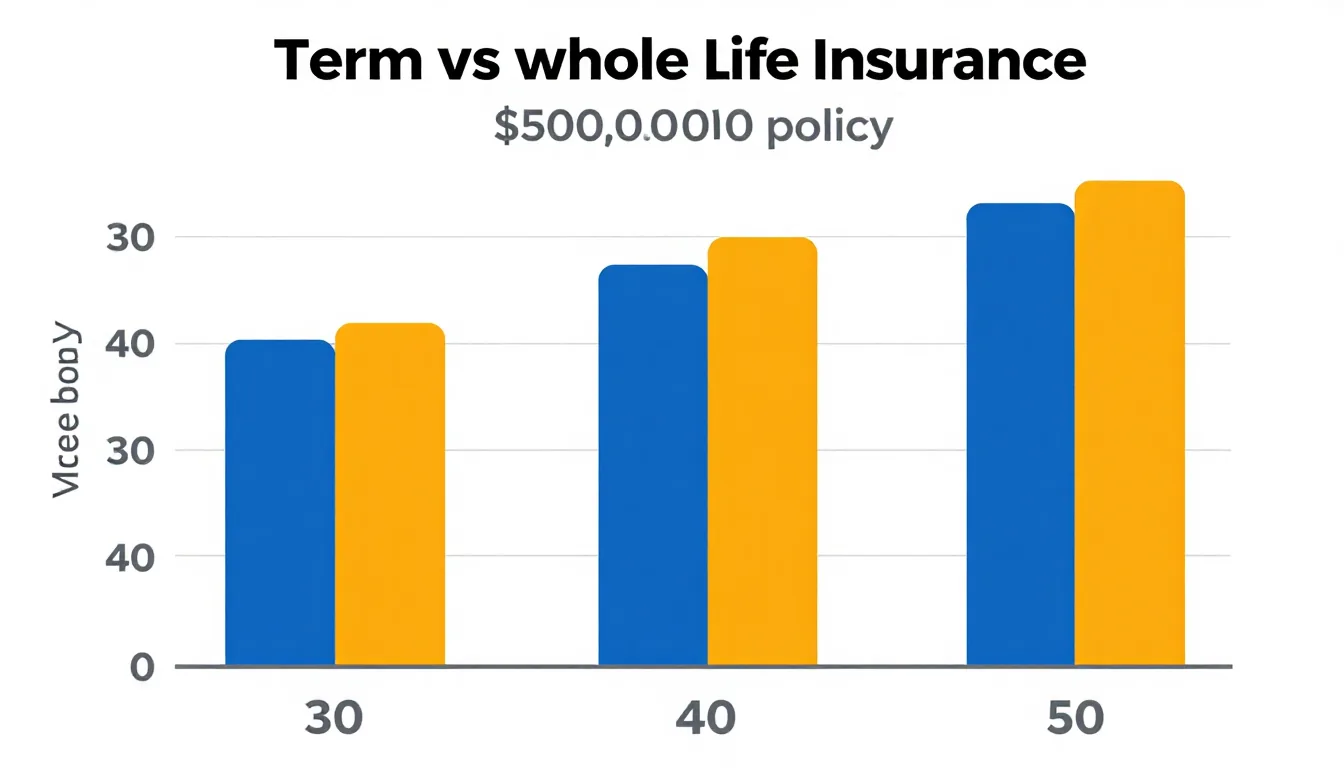

Most financial advisors recommend term for young families. A healthy 30-year-old can get a $500,000, 20-year term policy for roughly $30 per month.

That's a fraction of whole life costs. Term policies are ideal for covering specific obligations like a mortgage or college tuition.

How Whole Life Insurance Works

Whole life combines a death benefit with a cash account that grows tax-deferred. Premiums are much higher, but the policy never expires.

Over time, you can borrow against the cash value or withdraw it.

Whole life policies are often sold as “forced savings,” but they come with high fees and low returns. According to the Consumer Financial Protection Bureau, whole life premiums can be 10 to 20 times more than term for the same death benefit. The cash value grows slowly in the early years, making it a poor short-term investment.

Key Differences at a Glance

Cost Comparison

Term insurance is dramatically cheaper. A $250,000 term policy for a 35-year-old might cost $20–$40 per month.

Whole life for the same amount could run $200–$400 monthly. The premium difference widens with age and health.

When comparing term vs whole life, the cost gap is the most obvious factor. Over 20 years, the savings from choosing term can be invested elsewhere.

That's a key reason why term often wins for pure protection.

Investment Component

Whole life includes a cash value that earns a guaranteed interest rate, typically 2–4%. But that return is often less than what you'd earn in a simple index fund.

Term leaves you free to invest the savings elsewhere.

As Investopedia explains, the cash value grows slowly in the early years because of high upfront fees. It can take 10–15 years to break even. Meanwhile, investing the premium difference in a low-cost ETF could yield much higher returns over time.

Flexibility and Duration

Term policies expire. If your needs change—say, you stop needing coverage—you simply stop paying.

Whole life stays in force as long as you pay premiums, but you're locked into high payments for decades.

Some whole life policies allow you to reduce the death benefit or adjust premiums, but these options are limited. Term policies are simpler and more flexible for changing life stages.

The term vs whole life decision often hinges on how long you need coverage.

Pros and Cons of Each Policy Type

Term Life Pros

- Lowest premiums for maximum coverage.

- Simple and easy to understand.

- No cash value means no complex fees.

- Renewable and convertible options available.

Term Life Cons

- No cash value or investment component.

- Coverage ends after the term; renewal may be expensive.

- If you outlive the term, you get no benefit.

Whole Life Pros

- Lifetime coverage as long as premiums are paid.

- Cash value grows tax-deferred and can be borrowed against.

- Premiums are fixed and predictable.

- Useful for estate planning and wealth transfer.

Whole Life Cons

- Very high premiums compared to term.

- Low investment returns after fees.

- Complex policy features and surrender charges.

- Long break-even period (10–15 years).

Which One Should You Choose?

When Term Life Wins

- You need affordable coverage for a specific time period (e.g., until kids graduate).

- You want to maximize coverage per dollar spent.

- You’re comfortable investing the premium difference yourself.

When Whole Life Might Make Sense

- You have a high net worth and need estate tax planning.

- You want a guaranteed cash value component regardless of market conditions.

- You’ve maxed out other tax-advantaged accounts and want permanent coverage.

For 95% of people, term life is the better choice. It's simpler, cheaper, and allows you to invest the difference.

Whole life is a product designed for niche situations—not a one-size-fits-all solution.

Before buying any policy, compare quotes from multiple insurers. Check reviews and financial strength ratings.

And remember: life insurance is about protecting your family, not building wealth. Keep that focus.

The term vs whole life decision ultimately depends on your financial goals and budget.

For more guidance on personal finance, visit our Personal Finance section.